There is a new rule under the “Ease of Paying Taxes Act” to address VAT on uncollected receivables. This legislation allows businesses to claim back the VAT they paid on sales where they haven’t received payment. Below is a detailed breakdown of what this means and how it works.

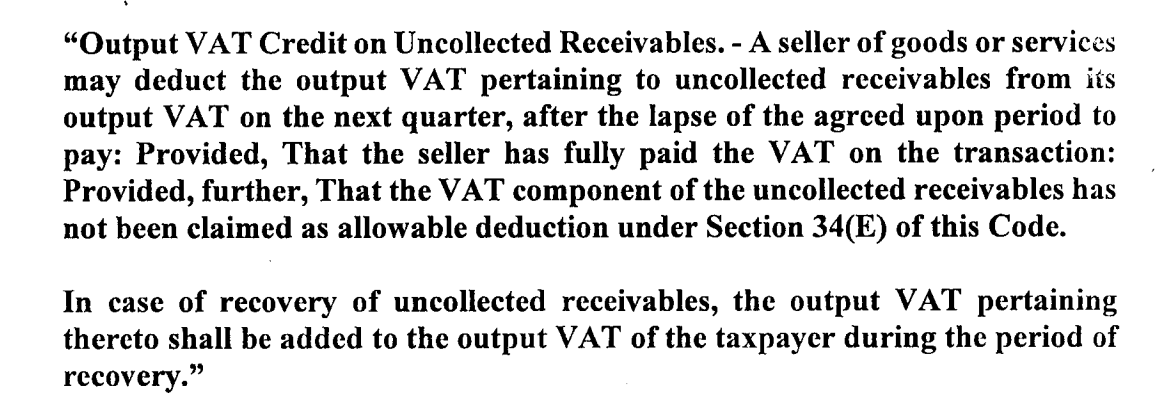

This is Section 110(D)

Output VAT Credit on Uncollected Receivables

A seller can deduct VAT on unpaid receivables from their VAT obligations in the next quarter, provided they have paid the VAT on that transaction and haven’t claimed it as a bad debt deduction.

What is the Rationale behind this?

This is to provide relief to sellers who are burdened with paying VAT on sales where the buyer hasn’t paid. In cash sales, sellers receive the full payment, including VAT, which they can then remit to the government. In credit sales, sellers must pay VAT upfront despite future payment promises. If receivables remain uncollected and are recognized as bad debts, the seller still pays the VAT without receiving sales proceeds.

What does “after the lapse of the agreed upon period to pay” mean?

This phrase means that the buyer agreed to pay for goods, services, or leased property within a specific time frame, as stated in a written agreement. If this time frame (or any extended time frame) has passed, and the buyer still hasn’t made the payment, this condition is met.

Who can claim or deduct output VAT credit on uncollected receivables?

Only the seller of goods or services can claim the output VAT credit for receivables that haven’t been paid. This applies to sales on credit made after the new rules (RR No. 3-2024) took effect. The seller can deduct this VAT from their next quarter’s VAT after the payment period has passed without payment.

Conditions on uncollected receivables in VAT

To be entitled to VAT credit, the following requisites must be present:

- The sale or exchange has taken place after the effectivity of RR No. 3-2024.

- The sale is on credit or on account.

- There is a written agreement on the period to pay the receivable, i.e. credit term is indicated on the invoice or any document showing the credit term.

- The VAT is separately shown on the invoice.

- The sale is specifically reported in the Summary List of Sales covering the period when the sale was made and not reported as part of “various” sales.

- The seller declared in the BIR Form No. 2550Q or the quarterly VAT Return (QVR) the corresponding output VAT indicated in the invoice within the period prescribed under existing rules.

- The period agreed upon, whether extended or not, has lapsed; and

- The VAT component of the uncollected receivable was not claimed as a deduction from gross income (i.e. bad debt) pursuant to Section 34(E) of the Tax Code.

Do these rules impact bad debt deductibility for income taxes?

No, these rules do not change the conditions for deducting bad debts on income tax returns, as specified in RR No. 25-2002. To claim the output VAT credit on uncollected receivables, the seller just needs the agreed payment period to have passed without payment. The seller doesn’t need to make any efforts to collect the receivables to be eligible for the VAT credit, as long as they meet the other conditions outlined earlier.

Should the seller automatically credit VAT for uncollected receivables due to payment period lapses?

No, claiming the VAT credit for uncollected receivables is optional for the seller. If the seller believes that the payment is likely to be collected eventually, they may choose not to claim the VAT credit immediately. This approach can save the seller from the hassle of claiming the VAT credit only to reverse it later if the receivable is eventually paid.

Can the seller claim VAT credit on uncollected receivables?

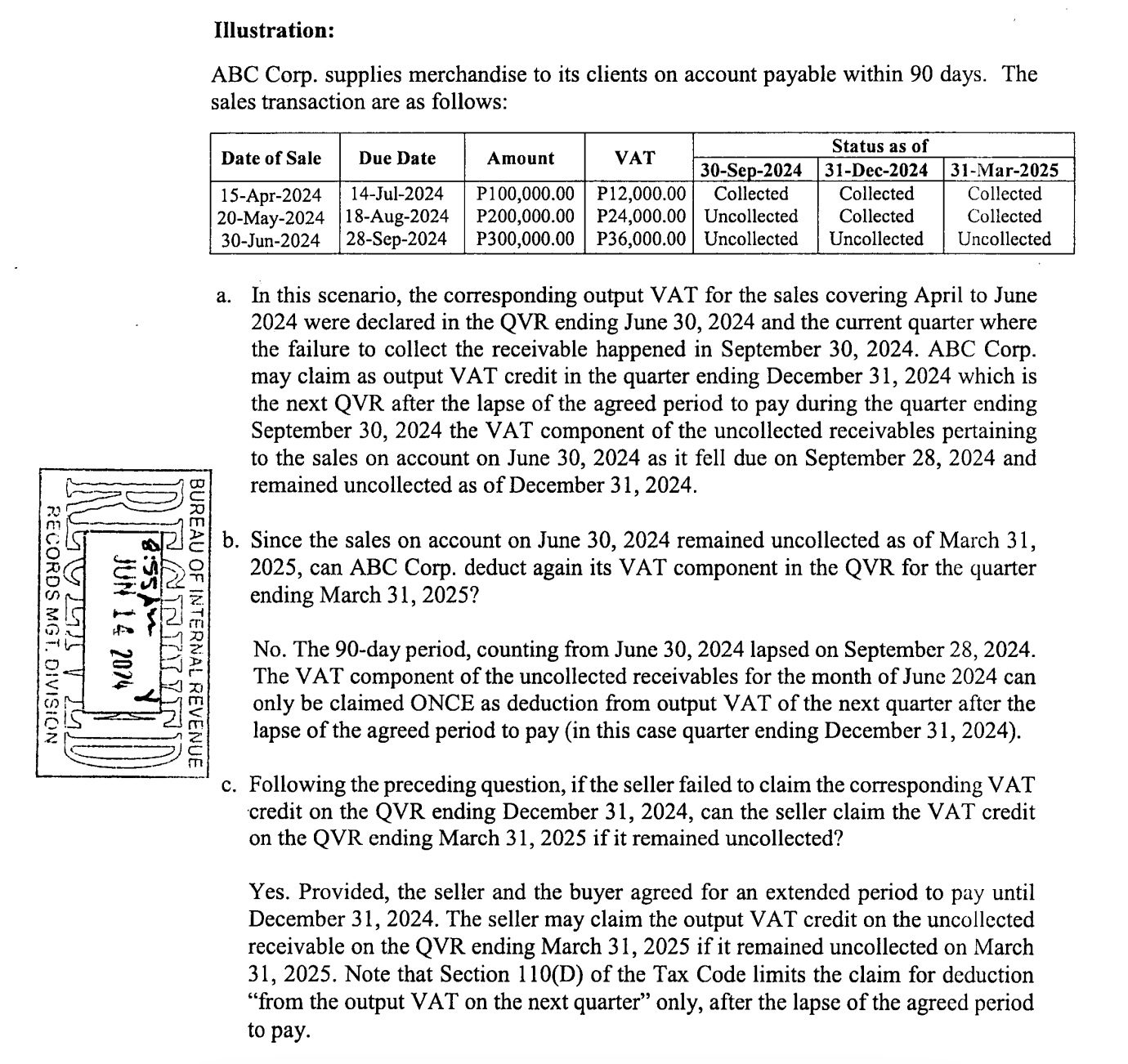

The seller can claim the output VAT credit on uncollected receivables in the next quarter after the agreed-upon period for payment has passed. This is mandated by Section 110(D) of the Tax Code.

To illustrate, taking this example from the IRR:

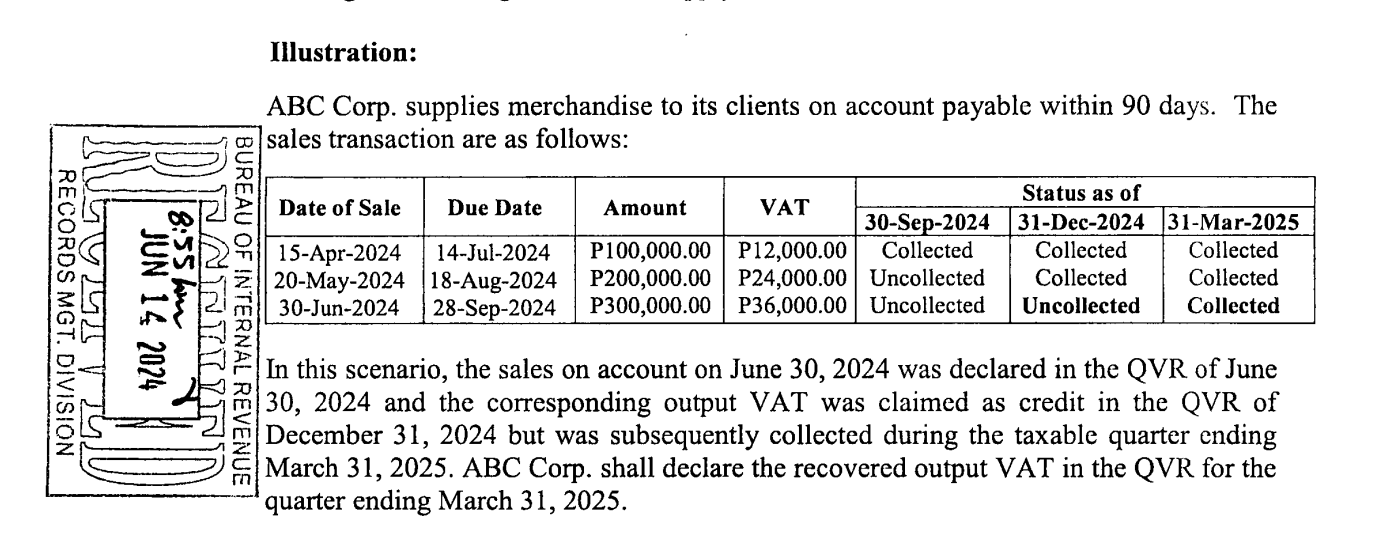

What if uncollected receivables are later recovered after claiming VAT credit?

If the seller recovers or collects the receivables for which they had previously claimed a VAT credit, they must report and declare the recovered VAT in the tax return for the quarter in which the recovery or collection occurred. If the seller fails to declare this, they may face penalties according to existing rules and regulations.

What is the effect on the buyer’s input tax when the seller claims output VAT credit on uncollected receivables?

When the seller claims an output VAT credit on uncollected receivables, the buyer can no longer use the corresponding input VAT as a credit. The input VAT claimed by the buyer will be disallowed once the seller claims the output VAT credit on the uncollected receivable.

How will the seller document sales with claimed output VAT credit for uncollected receivables?

The seller needs to stamp “Claimed Output VAT Credit” on their copies (duplicate/triplicate) of the invoice for the uncollected receivable. If there is a partial payment, the collected amount and the remaining uncollected balance should be noted. The seller can also issue additional documents like a credit memo or credit note, stating “Claimed Output VAT Credit” and referencing the original invoice. These documents will serve as proof and should be recorded in the seller’s accounts.

Is the seller required to provide the buyer a copy of the invoice stamped with the phrase “Claimed Output VAT Credit” and credit memo or credit note to the buyer?

Yes, the seller must provide the buyer with copies of the stamped invoice and any credit memo or credit note. This allows the buyer to adjust their claimed input VAT accordingly. If the seller fails to provide these documents, the buyer can voluntarily reverse their claimed input VAT credit in their Quarterly VAT Return (QVR).

What are the implications if the buyer failed to deduct accordingly in the available input taxes in its QVR the corresponding input VAT from the unpaid account from the seller?

If the buyer fails to properly adjust and deduct the input VAT from the unpaid account in their Quarterly VAT Return (QVR), they will be responsible for paying the deficiency VAT, including any applicable penalties. This will be enforced if the discrepancy is discovered during an audit by the Bureau of Internal Revenue (BIR) or if the buyer decides to amend their QVR to make the necessary adjustments.

Declaring output VAT credit

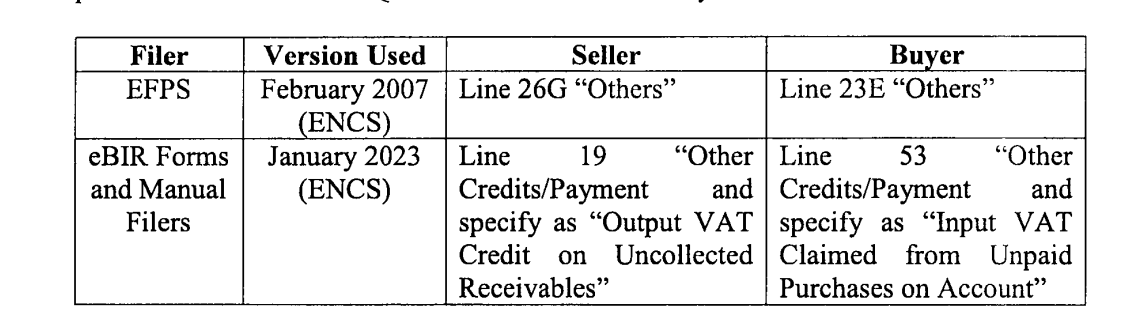

As an interim measure until a new version of the BIR Form No. 2550Q is released, the output VAT credit should be presented or declared in the seller’s and buyer’s Quarterly VAT Return (QVR) as follows:

- For the seller:

- On the EFPS (Electronic Filing and Payment System) using the February 2007 (ENCS) version, it should be reported under Line 26G “Others.”

- On eBIR Forms and for manual filers using the January 2023 (ENCS) version, it should be reported under Line 19 “Other Credits/Payment” and specified as “Output VAT Credit on Uncollected Receivables.”

- For the buyer:

- On the EFPS using the February 2007 (ENCS) version, it should be reported under Line 23E “Others.”

- On eBIR Forms and for manual filers using the January 2023 (ENCS) version, it should be reported under Line 53 “Other Credits/Payment” and specified as “Input VAT Claimed from Unpaid Purchases on Account.”

How should the sale be declared on the Summary List of Sales?

The customer or buyer must be clearly identified in the Summary List of Sales for the quarter when the sale was made. If the seller lumps all sales into a single “various” account entry, this will not comply with the requirements for claiming the output VAT credit on uncollected receivables. The VAT credit will not be allowed if the sale is not properly identified and remains uncollected after the payment period has passed.

Who are not qualified to avail the tax credit on VAT paid on uncollected receivables?

The following taxpayers are not eligible to claim the output VAT credit on uncollected receivables:

- Those labeled as “cannot be located” (CBL) taxpayers.

- Those with filed complaints at the Department of Justice under the Run After Fake Transactions (RAFT) and Run After Tax Evaders (RATE) programs.

- Other taxpayers identified by the Commissioner.

What if goods are returned but output VAT is unpaid?

If the goods are returned within the agreed payment period, it is treated as a sales return. This means the return is deducted from the gross sales in the quarter when the goods were returned.

What if goods are returned and accepted after claiming output VAT credit?

If the goods are returned and accepted by the seller after the seller has already claimed the output VAT credit, it is treated as a sales return. However, for VAT purposes, there will be no deduction on sales and output VAT since the output VAT credit has already been claimed.

What are the implications if there is partial or full collection of the previously uncollected receivable for which output VAT credit had been claimed?

If the seller partially or fully recovers the previously uncollected receivable, the corresponding output VAT for the amount collected must be added back to the seller’s output VAT for the period in which the recovery occurred.

Should the seller issue an invoice upon recovering a previously uncollected receivable?

The seller is not required to issue a new invoice. Instead, the seller should stamp the original invoice with the phrase “Recovered” and indicate the amount collected, if it is a partial recovery, on their copies of the invoice.

The seller can also issue supplementary documents, such as a debit memo or debit note, stating “Recovery of Previously Reported Uncollected Receivable” and referencing the original invoice. The seller must provide these documents to the buyer.

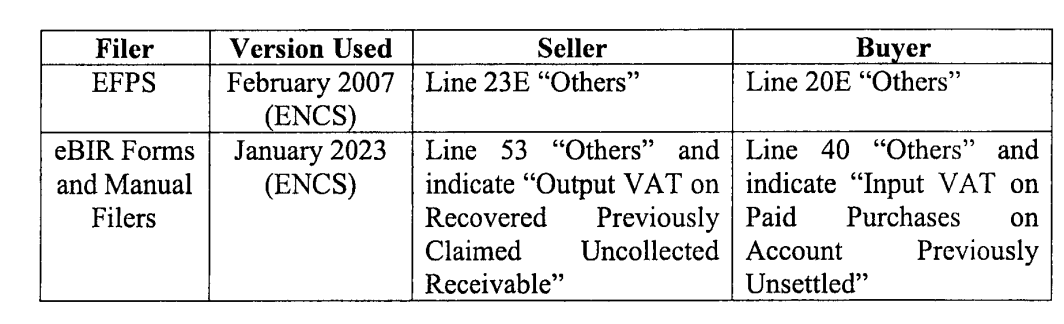

How should the output VAT of recovered or subsequently collected receivables be presented/declared in the VAT Return?

Until a new BIR Form No. 2550Q is released, the seller and buyer should reflect the output VAT in their VAT Returns as follows:

- For the seller:

- On EFPS (February 2007 version), report recovered output VAT under Line 23E “Others.”

- For eBIR Forms and manual filers (January 2023 version), report recovered output VAT under Line 53 “Others” as “Output VAT on Recovered Previously Claimed Uncollected Receivable.”

- For the buyer:

- On the EFPS using the February 2007 (ENCS) version, report the corresponding input VAT under Line 20E “Others.”

- For eBIR Forms and manual filers using the January 2023 (ENCS) version, report the corresponding input VAT under Line 40 “Others” and specify as “Input VAT on Paid Purchases on Account Previously Unsettled.”

Do outstanding receivables with declared output VAT qualify for output VAT credit under RR No. 3-2024, Section 110(D)?

No, the output VAT credit on uncollected receivables only applies to sales of goods and/or services on account that occurred after the effective date of RR No. 3-2024. Receivables from sales made before this date do not qualify for the VAT credit under Section 110(D) of the Tax Code.

Hope this article helps!

paano gumawa na tin id

Hello April,

Magrehistro sa BIR: Pumunta sa pinakamalapit na Revenue District Office (RDO) at dalhin ang valid ID at BIR Form 1901 (self-employed) o Form 1902 (empleyado).

Kumuha ng TIN: Bibigyan ka ng TIN matapos magrehistro.

Mag-request ng TIN ID: Pumunta muli sa RDO at mag-fill out ng request form. May fee na maaaring kailanganin.

Hintayin ang TIN ID: Karaniwang matatanggap ito pagkatapos ng ilang araw.

Kung may tanong ka, huwag mag-atubiling magtanong!